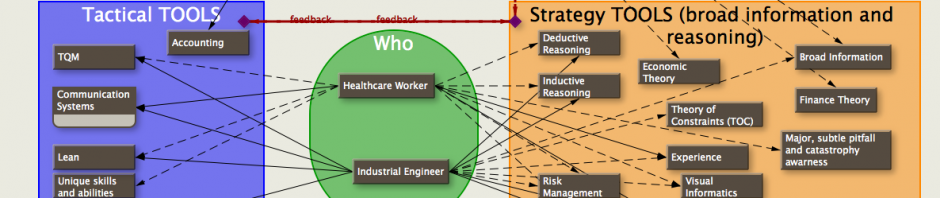

see also: TA (throughput accounting) and TDABC (time driven activity based costing)…the fabric, the ‘warp and woof’ of healthcare accounting?

from a Linkedin topic:

Just thought I’d expand on some thoughts about Acitivity Based Costing (ABC) vs Thoughput Accounting (TPA): [not quite sure how TDABC is handled]

Idea of TOC:

Optimize the application of resources (with many abilities) to any or all activities to achieve a goal.

=(resource x activity) cross product

Parameters of throughput goal:

(1) Defined goal/purpose/gain

(2) Time period (this month, this year, this life, life of planet) of this goal

(3) Risk your willing to take of running out of specific resources during that time period (some resource shortages merely cause delays, others such as cash or oxygen could cause the end)

This makes an accounting system a little more complicated. The “resource x activity” refers to the cross product of the resource and activity. That means that you need to keep track of both at the same time if you’re trying to improve things.

So, in my view, Activity Based Accounting is a simplified view of TPA. The parameters 1,2,and 3 are essential to TOC and hence TPA. You might also assume that parameters 2 and 3 can include the concepts of real options (hellaciously branching decision trees) that require a good bit of strategizing.

Then again, isn’t top management supposed to be ‘strategizing’ all the time? If so, then TPA would be the act of carrying the strategy down to the process level on an informed basis (sure…let administration run the machines:).

It looks as though true TPA would require more coordination and transfer of information from the people actually designing and doing the processes and the administration strategizers. ABC would not require such coordination of effort, and might not consider parameters 1,2, and 3 adequately (inadequate strategizing).

——-

continuing…

If the goal of TOC is to maximize cash flow, then TPA should correlate with the cash flow in the company.However, it’s conceivable the the TOC goal is something other than maximizing cash flow (charity?, or ::ROFL:: not-for profit hospital!), in which case you’ll still have to maintain sufficient cash flow to stay in business (unless you’re the VA).Often it seems that current hospital cost accounting does not appear to emphasize cash flow…nor charity…nor long term patient health. I’m not sure what the strategy is…nor if the strategy is frequently reevaluated.

———

continuing…

The goal in TOC would determine the clumping of actions into activities. Different goals can easily imply a different set of actions that lead to specific activities and the measured TPA activity expenses and revenues would change accordingly.This means that a ‘randomly’ set up definition of activities for ABC might, or might not, jive with the TPA system. Same goals, though, could cause ABC and TPA to be indistinguishable in effect.

———

continuing…

Paul- So I agree with you that a partial implementation of TOC/TA would be less than optimal for the hospital as a whole. But…there will be politics everywhere –the GI department will have a goal that is more aligned with the gastroenterologist, the pulmonology department will have a goal more aligned with that of the pulmonologist, etc. The goal may still be cash flow…but whose cash flow? Throughput accounting could be used to quantify by cash flow how far the goals of a particular department veer from those of the hospital, and what or who is the cause. Negotiations could ensue: possible recognition of the amount of loss in the potential total economic return, and ways to indirectly share income. An example is that of paying surgeons to cover surgical call. Ten years ago I remember a hospital claiming (in the newspaper) that a group of neurosurgeons was holding it hostage by demanding to be reimbursed for coverage (the group of three covered three hospitals every night with no reimbursement). Nowadays, compensation for call is the norm. Another example is guaranteed income for anesthesiologists who wander all over the hospital expediting sedations, intubations, epidurals, doing medicaid/medicare cases etc. for which they often are poorly directly reimbursed, but for which the hospital makes lots of money (eventually).

——–

continuing…

Robert Gordon • Brian,This last string of your comments has brought a whole new ray of enlightenment into the dusty loft of my mind. As we have discussed elsewhere, stereotypical healthcare activity essentially value-optimizes intra-operative decision making above the reduction of process variability. You have here made me remember and better understand something I was working on a couple of years ago, namely, the fact that the main value killer (“waste” for Lean) occurs in transitions or hand-offs during hospital care, both within and among disciplinary siloes. [I believe you are well aware that this process “articulation” is the focus of research and experiments in process modelling, DEM.] But the fact that transitions are a problem in hospital care probably has a homolog in the inescapable variability of healthcare processes. You say TOC (but QI methodologies in general) try to aggregate “actions into activities”. That is because of the all-unifying Goal. But in health/hospital care, there is no “goal” in this sense. You could say that the “Goal” of healthcare (health) is transcendent and equally present to every action, but that really just shows that “goal” is not the right concept. Ooo! it is all coming together! Thanks.

About Brian D Gregory MD, MBA

Board Certified Anesthesiologist for 30 years. TOC design and implement for 30 years.

MBA from U of Georgia '90: Finance, Data Management, Risk Management.

Practiced in multiple US states and Saudi Arabia at KFSH&RC and KFMC

Taught residents in two locations. Worked with CRNAs for 20 years.