“If discussing shop with a Finance person, one thought is to get a feel of where they are coming from. How difficult is it to get them to use “GAAP” in the conversation and what is their attitude about it?”

GAAP is used for financial reporting and should not be used for managerial accounting. A CPA uses GAAP, but a CMA ( IMA – Institute of Management Accountants ) doesn’t. CMAs run industries, CPAs make the industry look good to investors (my opinion), try to decrease taxes, and try to get big bonuses for the top executives. Also, GAAP is slowly being phased out to a similar, though different, standard used in many other countries.

“The US GAAP provisions differ somewhat from International Financial Reporting Standards, though former SEC Chairman Chris Cox set out a timetable for all U.S. companies to drop GAAP by 2016, with the largest companies switching to IFRS as early as 2009.”

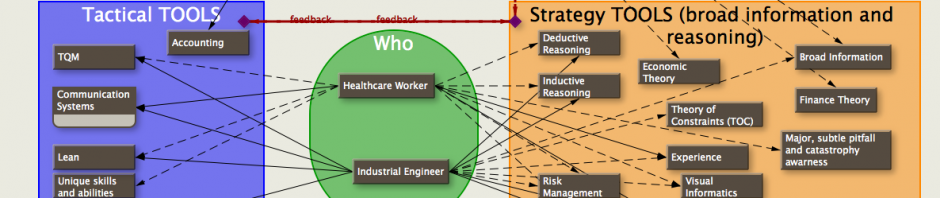

In your finance department, if you deal with someone who does not take a managerial accounting approach (a throughput account approach would also be good), you’ll have some difficulty communicating with them. In any event, the focus should be on increasing cash flow for the company as a whole, which usually is accomplished by increasing throughput and decreasing cost through all the various techniques (constraint theory, lean, TQM, etc) that operations management people have been trained to do. A CMA (more than a CPA) knows that operations people are integral to changing the cash flow. Whatever the cash flow, the CPA for the hospital can still manipulate the numbers to alter a profit & loss statement more to his liking… but more easily if there is increased cash flow. Cash flow, itself, (free cash flow and other variants) is not as easily manipulated. Also, without positive cash flow, the hospital tanks no matter what the income statement shows.

So, assuming the hospitals accounting is organized by departments and then consolidated for the hospital, you need to get the statements for each department and show how your operations management techniques can change the amount on line items of each department’s statement. Sometimes that line item will be independent, and sometimes it will be a proportion of an overhead cost to the hospital. Even if it’s a proportion of an overhead cost, if you can show how your technique decreased that proportion.

Take a department, or subset of a department, and see if you can alter its productivity or costs through any of your techniques. (You’ll need to interact with the people actually doing the work in that department to see what would be useful, and I suspect there are at least a few people within that department who would be happy to tell you what is needed.) Get with the finance department and see how much your technique could affect cash flow for that department. Then see how much it would affect productivity and cash flow in other departments. (Caveat: Alexander Kolker described at Children’s Hospital of Wisconsin shows a simulation on increased ER throughput which served to only move the bottleneck to the ICUs and ORs. So unless those departments also improve, there is not much advantage in ‘leaning up’ the ER.) There should be line items in the accounts for each department that would be directly affected by these changes.

[Line items (accounts) are by their nature very gross means of analyzing cause and effect. An account operates as a single number that is the result of a multivariate interaction. Compare an account (simple categorical grouping) to analyses that are done in operations management to discover cause and effect: analysis of variance, linear regressions, statistical grouping/clustering. So a line item would not be a good means of identifying the exact strategy or technique (TQM, lean, constraint) you used to cause the change, but you need it to be specific enough to show that YOU caused the change.]

Or…

Take a look at the accounts for departments that have a lot of interaction. Get with those departments and ask them what changes would help them work together better. If there’s nothing in the chart of accounts (line items) for those departments that would be affected by improving those interactions, it may be that the finance department’s chart of accounts needs tweaking. Maybe they need a new line item to adequately notice (in the way they’re accustomed to noticing) the positive effect you can create. It would give you a chance to ‘educate’ the finance department about operations.

So, try to set up the situation where you can affect the line item accounts of individual departments (services) within the hospital. You may also be able to have the finance department create or alter some line items to more adequately represent cost centers. Ideally, you’ll find some simple change in a department (or process) that has dramatic effects on accounts throughout the hospital. Another way to look at this is that all those people in various departments who know there’s a ‘better way’ need a sponsor (you) who can interact with the heads of the hospital (through your operations and financial expertise) and cause positive changes.

—————

Lean accounting, throughput accounting and others…

Returning to the concept of ‘Tell me what you measure, and I’ll tell you what they do’, lean accounting is a technique that attempts to focus the attention of the accountants more on process…and process converts to money. There are other approaches to accounting that focus on important factors such as throughput accounting.

Throughput accounting focuses on bottlenecks. According to throughput accounting, if you’re not ‘leaning’ the right thing, you’re wasting your time (not exactly true, but you get the idea).

You could design an accounting system…let’s call it ‘marginal accounting’… in which you keep track of the marginal contribution to revenue from a secondary process (decide what the primary process should be with constraint theory). Pick the secondary (marginal) product that makes use of any capacity under utilization or waste products from the primary activity that returns the most money. Michaelangelo could have made extra money selling gravel from the chips off his David. If he’d tried to profit from focusing on gravel first, he’d have been much poorer and less famous. So in ‘marginal accounting’, sequence matters.

How about one more system…let’s call it ‘opportunity cost accounting’. In opportunity cost accounting, you keep track of how much money you didn’t make by not taking advantage of changing situations (opportunities). This would make management pounce on new opportunities as soon as they arise. No more ‘business as usual’, because it would become apparent immediately in the accounting statements (and they’d be fired).

The point is that accounting needs to evolve faster, provide better information at some level, and help improve decision-making and processes instead of hindering them. A proper accounting system will help you make better decisions, but the bottom line…the cash flow… will be in all of them, and that’s the final score.